At first glance, it seems reasonable to expect Intel (NASDAQ:INTC) stock to rally this year since it manufactures AI chips like the ARC A770, A750, and A580 lineups priced at an attractive range.

However, the stock is down 38% year-to-date in a year that tech stocks are rallying. Intel’s valuation is still high despite U.S. government support, weak finances, and declining market share in key areas.

Governmental Funding Provides The resources It Needs To Grow

The U.S. government would like Intel to remain a strong player in the semiconductor industry compared to other emerging Chinese companies.

In March 2024, Intel announced its plans with the U.S. government under the CHIPS Act, which proposed more than $100 billion in the U.S. semiconductor chip industry over the next five years and $8.5 billion directly to Intel.

To better understand the funding scale, Intel had less than $2 billion in net income last year. One of the key ways Intel plans to use this funding is to develop its AI capabilities, which means that this funding can help it catch up to competitors in AI chips, such as Nvidia (NASDAQ:NVDA) and Advanced Micro Devices (NASDAQ:AMD)

U.S. politicians seem to believe in this, too. In May 2024, Congressman Michael McCaul purchased Intel stock worth an estimated $250,000 to $500,000.

Furthermore, he is the co-chair and Founder of the Congressional High Tech Caucus and helped write the CHIPs Act. His purchase is a bullish sign that this program could significantly help Intel.

Losing Market Share

One of the biggest reasons I don’t want to gamble on Intel is that it has lost its market share in its core market with no indication of a comeback. Its market share in desktop CPUs declined again in 2024, with 76.1% versus 80.8% in quarter 1 of 2023, as it continues to lose to AMD.

In addition, it lost out to ARM (NASDAQ:ARM), when Apple (NASDAQ:AAPL)’s computers stopped using Intel in 2020. The same is happening with some PC laptops and Chromebooks as well.

Microsoft’s (NASDAQ:MSFT) new PCs, which will have AI functions heavily implemented natively, are set to mainly deliver with ARM-based chips due to their power efficiency while beating out Intel’s speed.

Valuation Isn’t Justified

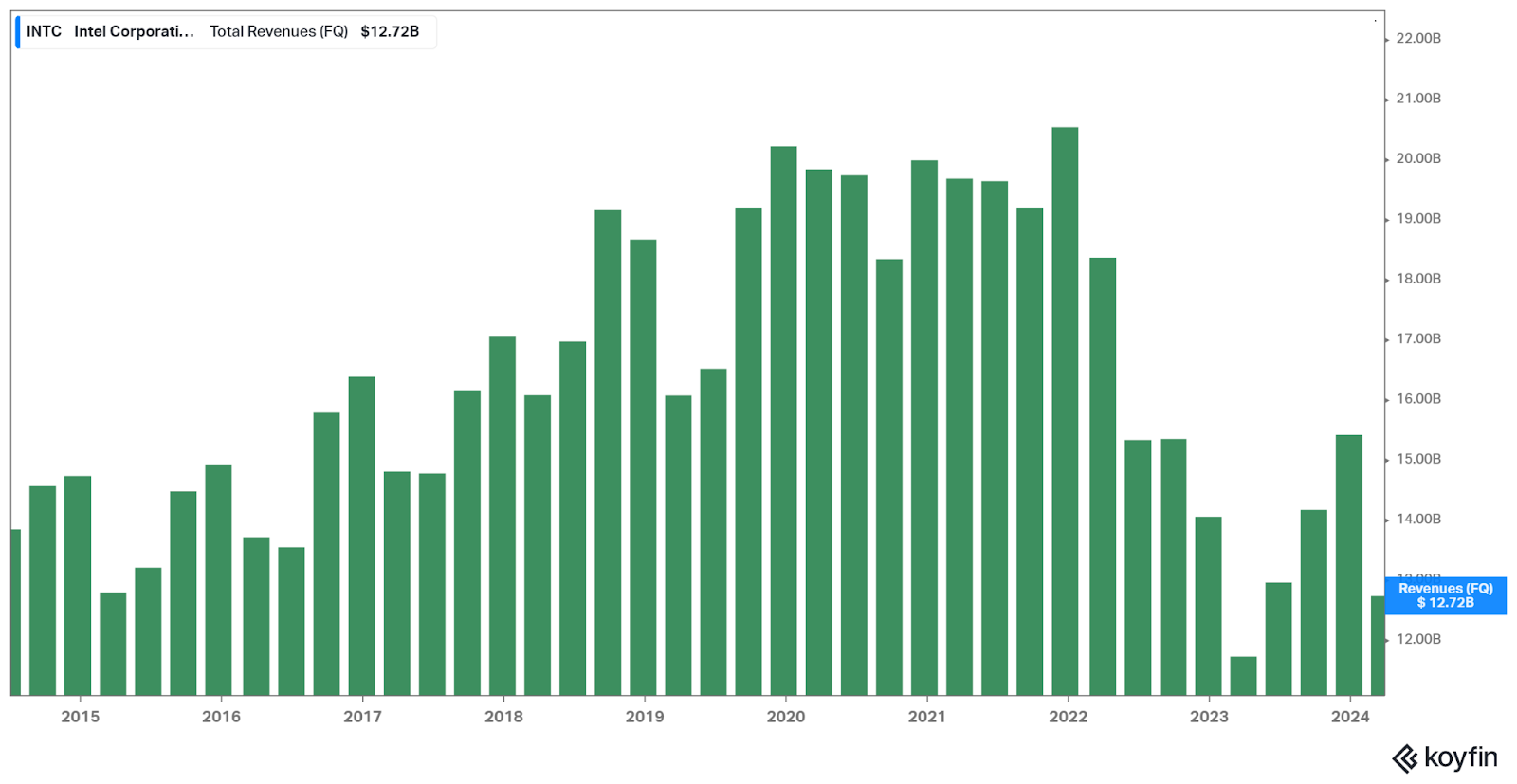

As a result of its failure to catch up with the rest of the market, Intel’s revenue has tanked. The chart below shows its revenue at $12.72 billion in the latest quarter, which has fallen off a cliff compared to when Intel would make north of $20 billion a quarter.

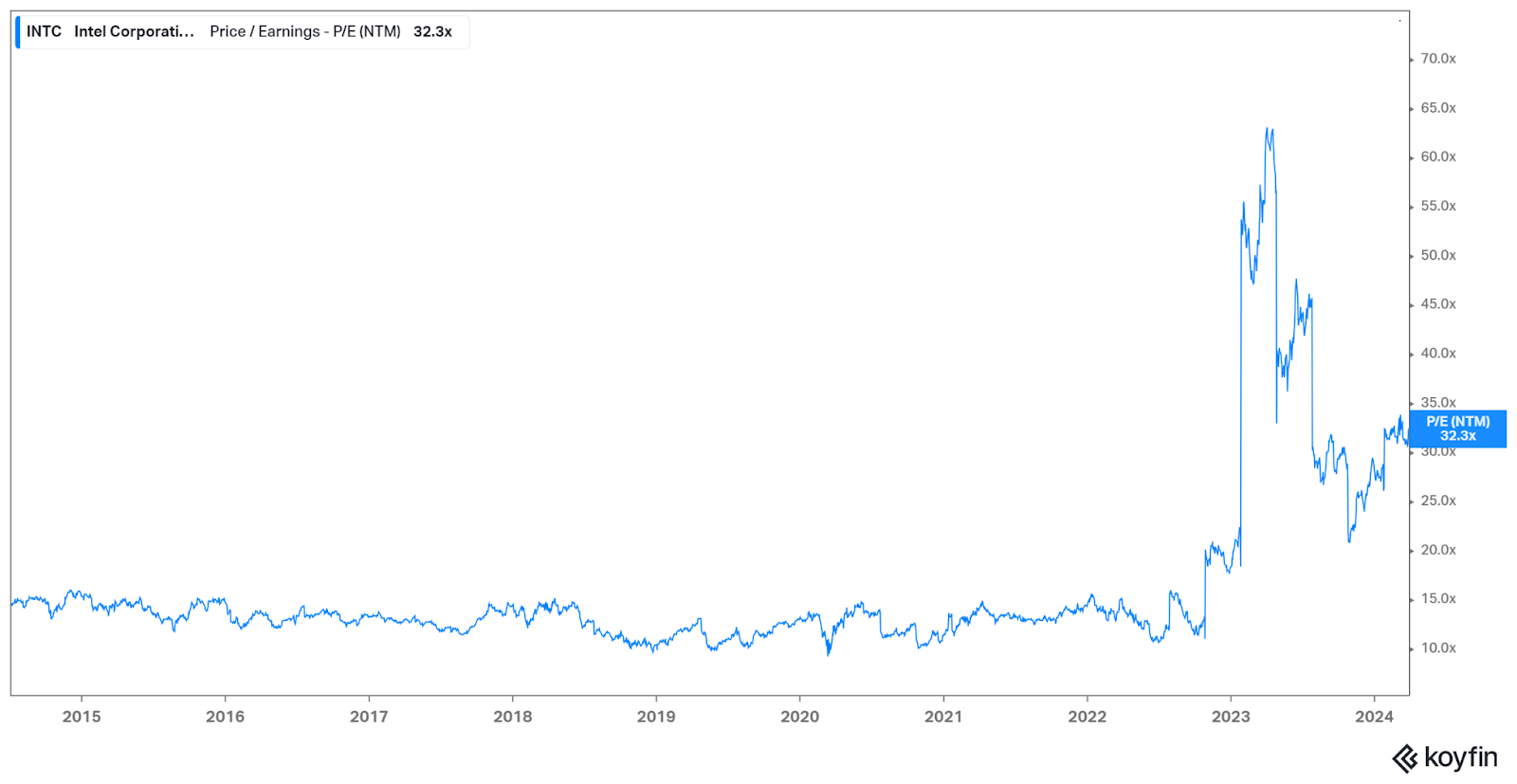

For a company that is seeing its revenue decline, its valuation only shot up. It’s currently trading at a forward price-to-earnings ratio of 32.3x, more than double the amount it was trading in 2022 and likely due to the AI craze.

However, as of 2024, it still only has 1% of the market share of AI chips, which has not meaningfully increased.

The company is being traded almost like a growth stock, while revenue growth has thus been negative, and its AI efforts show no signs of success.

My Verdict

AI is a catalyst for Intel, and maybe the federal government’s money could help it penetrate the AI chip market to warrant its current valuation, which is double before the AI craze 2022.

However, I don’t want to take this bet because it is losing customers in its core segment of desktop CPUs while its AI efforts have been mediocre.

I might’ve considered Intel if its valuation keeps coming down, but for now, buying into Intel is a pure gamble on AI that is already exceptionally priced, as seen in its jump in P/E.

On the date of publication, Michael Que did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

The researchers contributing to this article did not hold (either directly or indirectly) any positions in the securities mentioned in this article.