Over the last few trading sessions, SoundHound AI (NASDAQ:SOUN) fell by more than 12% from $6.20 a share to $5.49. For those who don’t follow SoundHound AI stock, the company makes AI voice assistants that can be used on everything from the phone in your hotel room to the drive-through at a fast-food restaurant.

Its technology has already been implemented at many well-known brands like White Castle, Hyundai (OTCMKTS:HYMTF), and Qualcomm (NASDAQ:QCOM).

Despite its recent decline, the stock price is still up over 160% year-to-date. These returns have outperformed Nvidia (NASDAQ:NVDA), who also happens to be an investor in the company.

In this article, I will explain the potential headwinds facing SOUN stock and my outlook for the rest of 2024.

Why Is SoundHound AI Stock Down?

As the stock has rallied, its valuation has been called into question. SoundHound AI stock trades at an Enterprise Value/Revenue multiple of 35.46x, while the median EV/Revenue multiple for private AI companies sits at 25.8x.

In addition, it was revealed that Chief Technology Officer Timothy Stonehocker sold over $1 million worth of SOUN shares on July 11, 2024, for $5.75 a share. While not always indicative of sentiment, large insider sales can reinforce the narrative that the stock is overvalued.

The recent announcement that SoundHound’s AI voice assistants were coming to sports bar chain Beef ‘O’ Brady’s should have been bullish for the stock.

However, the positive news may have been an opportunity for investors, especially those who were able to get in at less than $2.00 earlier this year, to take their profits.

SoundHound’s Risky Financials

Investors considering SoundHound stock should know that this is a high-risk and high-reward investment. The company is growing revenue at almost 50% year-over-year. Margins aren’t drastically improving and the company is losing more money every year. In FY 2024, SoundHound lost a total of $94.5 million

The company earned $11.6 million in Q1 2024 at the same time that R&D expenses alone were $14.9 million. This discrepancy suggests that there might be a long time before SoundHound breaks even and it’s very much in its hyper growth stage.

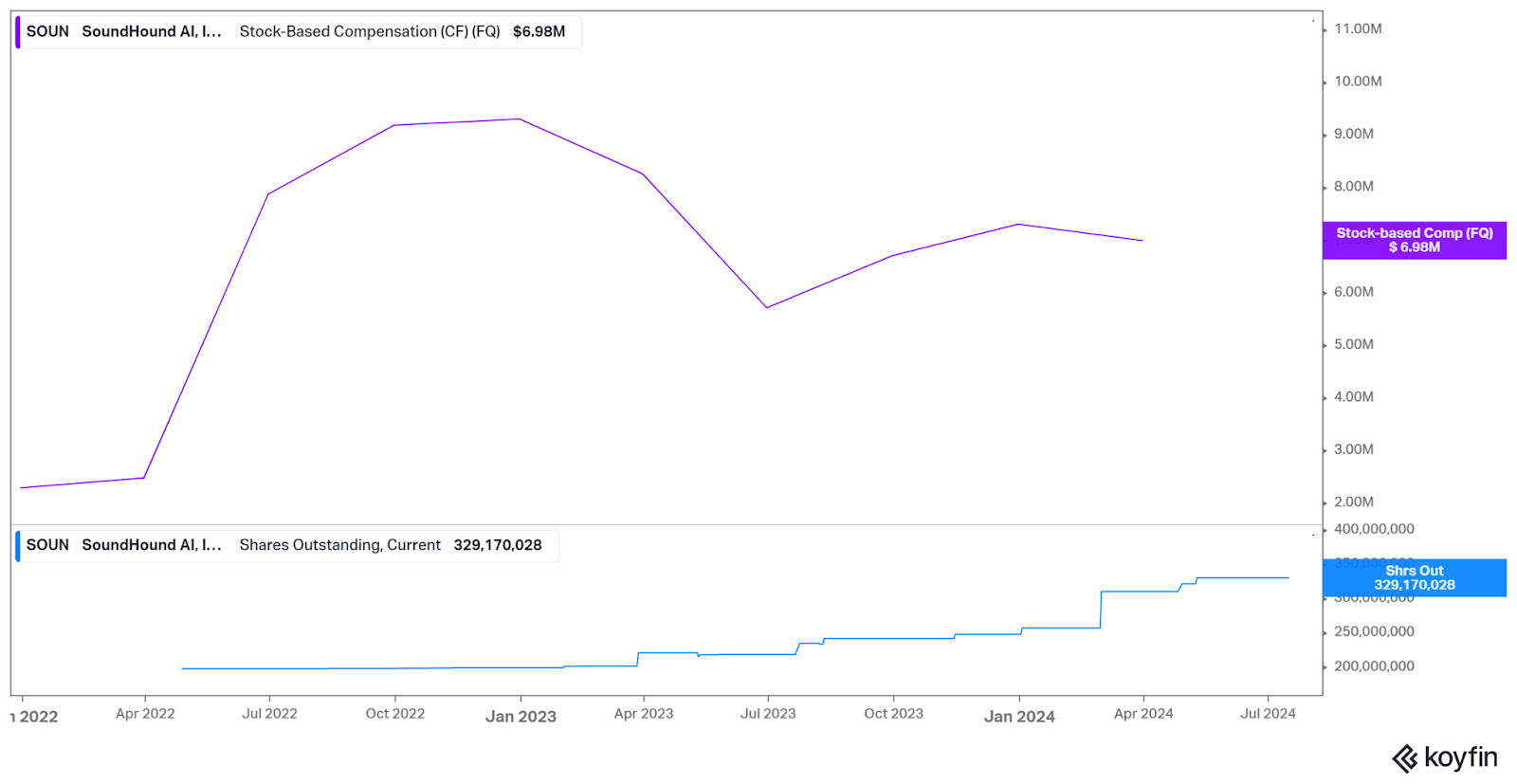

Investors investing at this stage might see their shares heavily diluted. Just in the last six months, over 1.3 million shares have been sold by the company while there were 343,000 additional shares that have been created from stock grants.

Stock-based compensation expenses continue to be high, clocking in at $6.98 million this quarter while shares outstanding also continues to increase.

Chart courtesy of <a href=”https://www.koyfin.com/“>Koyfin</a>

SOUN is a Buy if an Acquisition Seems Likely

With a growth stock like SoundHound, no one truly knows how successful the company will be. However, I believe that an acquisition of SoundHound is possible and could propel the stock higher depending on how the acquiring company values it.

The company has over 120 granted patents and is already working with many blue-chip and Fortune 500 companies. It’s also available in 25 languages and processes billions of queries per year, giving it lots of proprietary data to further train its AI model.

It’s estimated that just two customers made up of 48% of SoundHound’s revenue. We don’t know which companies they are, but high revenue concentration could mean one of those companies buying out SoundHound completely if it becomes integral to their business.

With a market cap of almost $2 billion, it isn’t overly expensive. Tech giants and AI pioneers like Google could easily afford SoundHound as seen by their recent AI transactions.

SoundHound is an interesting company, and its growing track record makes it a strong emerging AI player. Currently, a murky outlook for its long-term survival and a high valuation makes it too risky of an investment for my liking.

However, I will be watching closely on potential action regarding an acquisition of the company as I think it could be a prime target.

On the date of publication, Michael Que did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.